Government ing Manual For National Government Agencies 4w695u

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 445h4w

Overview 1s532p

& View Government ing Manual For National Government Agencies as PDF for free.

More details 6h715l

- Words: 3,676

- Pages: 14

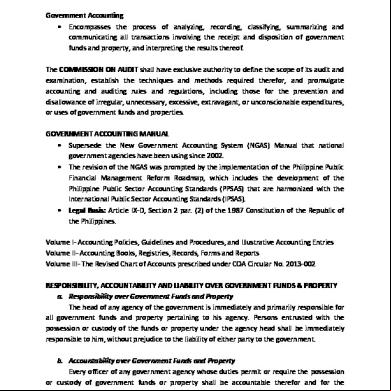

GOVERNMENT ING MANUAL FOR NATIONAL GOVERNMENT AGENCIES Government ing Encomes the process of analyzing, recording, classifying, summarizing and communicating all transactions involving the receipt and disposition of government funds and property, and interpreting the results thereof. The COMMISSION ON AUDIT shall have exclusive authority to define the scope of its audit and examination, establish the techniques and methods required therefor, and promulgate ing and auditing rules and regulations, including those for the prevention and disallowance of irregular, unnecessary, excessive, extravagant, or unconscionable expenditures, or uses of government funds and properties. GOVERNMENT ING MANUAL Supersede the New Government ing System (NGAS) Manual that national government agencies have been using since 2002. The revision of the NGAS was prompted by the implementation of the Philippine Public Financial Management Reform Roap, which includes the development of the Philippine Public Sector ing Standards (PPSAS) that are harmonized with the International Public Sector ing Standards (IPSAS). Legal Basis: Article IX-D, Section 2 par. (2) of the 1987 Constitution of the Republic of the Philippines. Volume I- ing Policies, Guidelines and Procedures, and Illustrative ing Entries Volume II- ing Books, Registries, Records, Forms and Reports Volume III- The Revised Chart of s prescribed under COA Circular No. 2013-002 RESPONSIBILITY, ABILITY AND LIABILITY OVER GOVERNMENT FUNDS & PROPERTY a. Responsibility over Government Funds and Property The head of any agency of the government is immediately and primarily responsible for all government funds and property pertaining to his agency. Persons entrusted with the possession or custody of the funds or property under the agency head shall be immediately responsible to him, without prejudice to the liability of either party to the government. b. ability over Government Funds and Property Every officer of any government agency whose duties permit or require the possession or custody of government funds or property shall be able therefor and for the

safekeeping thereof in conformity with law. Every AO shall be properly bonded in accordance with law. c. Liability over Government Funds and Property Expenditures of government funds or uses of government property in violation of law or regulations shall be a personal liability of the official or employee found to be directly responsible therefor. Every officer able for government funds shall be liable for all losses resulting from the unlawful deposit, use, or application thereof and for all losses attributable to negligence in the keeping of the funds. FUNDAMENTAL PRINCIPLES FOR REVENUE a. Unless otherwise specifically provided by law, all revenues accruing to an entity by virtue of the provisions of existing law, orders and regulations shall be deposited/ remitted in the National Treasury (NT) or in any duly authorized government depository, and shall accrue to the General Fund (GF) of the NG. b. Amounts received in trust and from business-type activities of government may be separately recorded and disbursed in accordance with such rules and regulations as may be determined by a Permanent Committee composed of the Secretary of Finance as Chairman, and the Secretary of Budget and Management and the Chairman, COA, as . c. Receipts shall be recorded as revenue of Special, Fiduciary or Trust Funds or Funds other than the GF, only when authorized by law as implemented by rules and regulations issued by the Permanent Committee. d. No payment of any nature shall be received by a collecting officer without immediately issuing an official receipt in acknowledgement thereof. FUNDAMENTAL PRINCIPLES FOR DISBURSEMENT OF PUBLIC FUNDS a. No money shall be paid out of any public treasury or depository except in pursuance of an appropriation law or other specific statutory authority. b. Government funds or property shall be spent or used solely for public purposes. c. Trust funds shall be available and may be spent only for the specific purpose for which the trust was created or the funds received. d. Claims against government funds shall be ed with complete documentation. BASIC GOVERNMENT ING AND BUDGET REPORTING PRINCIPLES a. Generally accepted government ing principles in accordance with the PPSAS and pertinent laws, rules and regulations; b. Accrual basis of ing in accordance with the PPSAS;

c. Budget basis for presentation of budget information in the financial statements (FSs) in accordance with PPSAS 24; d. Revised Chart of s prescribed by COA; e. Double entry bookkeeping; f. Financial statements based on ing and budgetary records; and g. Fund cluster ing. Keeping of the General s The COA shall keep the general s of the Government and, for such period as may be provided by law, preserve the vouchers and other ing papers pertaining thereto Financial Reporting System for the National Government a. Each entity of the National Government (NG) maintains complete set of ing books by fund cluster which is reconciled with the records of cash transactions maintained by the BTr. b. Each entity maintains budget registries which are reconciled with the budget records maintained by the DBM and the Government ancy Sector (GAS), COA. c. The COA, through the GAS: 1. Maintains budget records showing the overall approved budget of the NG and its execution/implementation; 2. Consolidates the FSs and budget ability reports of all NGAs and the BTr with COA’s records to come up with an Annual Financial Report (AFR) for the NG as required in Section 4, Article IX-D of the 1987 Philippine Constitution; and 3. prepares other financial reports required by law for submission to oversight agencies. Components of General Purpose Financial Statements a. Statement of Financial Position b. Statement of Financial Performance c. Statement of Changes in Net Assets/Equity d. Statement of Cash Flows e. Statement of Comparison of Budget and Actual Amounts f. Notes to the Financial Statements, comprising a summary of significant ing policies and other explanatory notes Books of s and Registries a. Journals 1. General Journal

2. Cash Receipts Journal 3. Cash Disbursements Journal 4. Check Disbursements Journal b. Ledgers 1. General Ledgers 2. Subsidiary Ledgers c. Registries 1. Registries of Revenue and Other Receipts 2. Registry of Appropriations and Allotments 3. Registries of Allotments, Obligations and Disbursements 4. Registries of Budget, Utilization and Disbursements FUND ING: FUND CLUSTERS Code 01 02 03 04 05 06 07

Description Regular Agency Fund Foreign Assisted Projects Fund Special -Locally Funded/Domestic Grants Fund Special -Foreign Assisted/Foreign Grants Fund Internally Generated Funds Business Related Funds Trust Receipts

OTHER PROVISIONS a. Fair Presentation b. Compliance with PPSASs. Explicit and unreserved statement of such compliance c. Departure with PPSASs. If compliance with the requirement of PPSAS would result in misleading presentation that it would contradict the objective of the FSs set forth in PPSAS. d. Going Concern. Unless there is an intention to discontinue the entity operation, or if there is no realistic alternative but to do so. e. Consistency of Presentation. Retained from one period to the next unless laws, rules and regulations, and PPSAS require a change in presentation. f. Offsetting. Assets and liabilities, and revenue and expenses shall not be allowed to offset unless required or permitted by a PPSAS except when offsetting reflects the substance of the transaction or other event.

g. Comparative Information. Comparative information shall be disclosed with respect to the previous period for all amounts reported in the FSs. Comparative information shall be included for narrative and descriptive information when it is relevant to an understanding of the current period’s FSs. Inclusions in the Statement of Changes in Net Assets/ Equity a. Net Income or Deficit for the period; b. Each item of revenue and expenses for the period that, as required by Standards, is recognized directly in net assets/equity, and the total of these items; c. Total revenue and expenses for the period; and d. For each component of net assets/equity separately disclosed, the effects of changes in ing policies and corrections of errors recognized in accordance with PPSAS 3ing Policies, Changes in ing Estimates and Errors. Statement of Comparison of Budget and Actual Amounts. A comparison of budget and actual amounts will enhance the transparency of financial reporting in government. This shall be presented by government agencies as a separate additional financial statement referred in this Manual as the Statement of Comparison of Budget and Actual Amounts (SCBAA). Use of Appropriated Funds. All moneys appropriated for functions, activities, projects and programs shall be available solely for the specific purposes for which these are appropriated. Appropriation for Loan Proceeds. Expenditures funded by foreign and domestic borrowings shall be included within the expenditure program of the entity concerned. Loan proceeds, whether in cash or in kind, shall not be used without the corresponding release of funds through a Special Budget. Basic Requirements for Disbursements and the Required Certifications a. Availability of allotment/budget for obligation/utilization certified by the Budget Officer/Head of Budget Unit; b. Obligations/Utilizations properly charged against available allotment/budget by the Chief ant/Head of ing Unit; c. Availability of funds certified by the Chief ant; d. Availability of cash certified by the Chief ant; e. Legality of the transactions and conformity with existing rules and regulations. f. Submission of proper evidence to establish validity of the claim. g. Approval of the disbursement by the Head of Agency or by his duly authorized representative.

Mode of Disbursements. Payments/Disbursements by NGAs may be effected through the Treasury Single (TSA), by issuing Modified Disbursements System (MDS) check or commercial check, cash through cash advance, Advice to Debit (ADA), or Non-Cash Availment Authority (NCAA). NGAs are authorized to disburse/pay based on the Notice of Cash Allocation (NCA), Notice of Transfer of Allocation (NTA), Cash Disbursement Ceiling (CDC) or other authority that may be provided by law. BUDGET EXECUTION, MONITORING AND REPORTING Allotment – is an authorization issued by the DBM to NGAs to incur obligations for specified amounts contained in a legislative appropriation in the form of budget release documents. It is also referred to as Obligational Authority. Appropriation – is the authorization made by a legislative body to allocate funds for purposes specified by the legislative or similar authority. Disbursements – are the actual amounts spent or paid out of the budgeted amounts. Obligation – is an act of a duly authorized official which binds the government to the immediate or eventual payment of a sum of money. Obligation maybe referred to as a commitment that encomes possible future liabilities based on current contractual agreement. FUND RELEASE DOCUMENTS a. Obligational Authority or Allotment 1. General Appropriations Act Release Document (GAARD) – serves as the obligational authority for the comprehensive release of budgetary items appropriated in the GAA, categorized as For Comprehensive Release (FCR). 2. Special Allotment Release Order (SARO) – covers budgetary items under For Later Release (FLR) (negative list) in the entity submitted Budget Execution Documents (BEDs), subject to compliance of required documents/clearances. Releases of allotments for Special Purpose Funds (SPFs) (e.g., Calamity Fund, Contingent Fund, E-Government Fund, Feasibility Studies Fund, International Commitments Fund, Miscellaneous Personnel Benefits Fund and Pension and Gratuity Fund) are also covered by SAROs. 3. General Allotment Release Order (GARO) – is a comprehensive authority issued to all national government agencies, in general, to incur obligations not exceeding an authorized amount during a specified period for the purpose indicated therein.

b. Disbursement Authority 1. Notice of Cash Allocation (NCA) – authority issued by the DBM to central, regional and provincial offices and operating units to cover the cash requirements of the agencies; 2. Non-Cash Availment Authority (NCAA) – authority issued by the DBM to agencies to cover the liquidation of their actual obligations incurred against available allotments for availment of proceeds from loans/grants through supplier’s credit/constructive cash; 3. Cash Disbursement Ceiling (CDC) – authority issued by DBM to the Department of Foreign Affairs and Department of Labor and Employment to utilize their income collected/retained by their Foreign Service Posts (FSPs) to cover their operating requirements, but not to exceed the released allotment to the said post; and 4. Notice of Transfer of Allocation – authority issued by the Central Office to its regional and operating units to cover the latter’s cash requirements. Registry of Appropriations and Allotments Shall be maintained by NGAs to monitor appropriations and allotments charged thereto. It shall show the original, supplemental and final budget for the year and all allotments received charged against the corresponding appropriation. Registries of Budget, Utilization and Disbursements Shall be used to record the approved special budget and the corresponding utilizations and disbursements charged to retained income authorized under R.A. 8292 for SUCs and other retained income collection of a national government agency with similar authority, Revolving Funds and Trust Receipts/Custodial Funds. a. Registry of Budget, Utilization and Disbursements-Personnel Services (RBUD-PS) shall be used to record the budget utilizations and disbursements classified under PS. b. Registry of Budget, Utilization and Disbursements-Maintenance and Other Operating Expenses (RBUD-MOOE) shall be used to record the budget utilizations and disbursements classified under MOOE. c. Registry of Budget, Utilization and Disbursements-Financial Expenses (RBUD-FE) shall be used to record the budget utilizations and disbursements classified under FE. d. Registry of Budget, Utilization and Disbursements-Capital Outlays (RBUD-CO) shall be used to record the budget utilizations and disbursements classified under CO.

Budget Utilization Request and Status. The incurrence of budget utilization shall be made through the issuance of Budget Utilization Request and Status (BURS). The BURS shall be prepared by the Requesting/Originating Office ed by valid claim documents like DV, payroll, purchase/job order, itinerary of travel, etc. Presentation of Budget Information in the Financial Statements on a Comparable Basis. An entity shall prepare a comparison of the budget and actual amounts spent as a separate statement since the budget and the financial statements are not prepared on a comparable basis in accordance with PPSAS Responsibility Center Code Structure. Each NGA shall be assigned a responsibility center code defined as organization code in the UACS Manual. For monitoring revenue and expenses, additional three digit codes for the agency’s major offices/departments shall be appended to the organization code. The organization code and the agency’s major offices/departments’ code shall consist of 15 digits as follows:

REVENUE AND OTHER RECEIPTS Unless otherwise specifically provided by law, all revenue (income) accruing to the departments, offices and agencies by virtue of the provisions of existing laws, orders and regulations shall be deposited in the NT or in the duly authorized depository of the Government and shall accrue to the General Fund of the Government: Provided, that amounts received in trust and from business-type activities of government may be separately recorded and disbursed in accordance with such rules and regulations as may be determined by the Permanent Committee. Revenue from Exchange Transactions 1. Rendering of services 2. Sale of goods 3. Interests 4. Royalties 5. Dividends or similar distributions Revenue from Non-Exchange Transactions a. Tax Revenue- Individual and Corporation, Property, Goods and Services, Others b. Fines and Penalties- Tax Revenue, Service Income, Business Income c. Shares, Grants and Donations- Share from National Wealth, Share from Philippine Amusement and Gaming Corporation (PAGCOR)/ Philippine Charity Sweepstakes Office (PCSO), Share from Earnings of GOCCs, Income from Grants and Donations in Cash, Income from Grants and Donations in Kind d. Revenues arising from Trust Liabilities, Deferred Credits, Unearned Revenue GRANT WITH CONDITION If conditions are attached to a grant, a liability is recognized. If the government is required to recognize a liability in respect of any conditions relating to assets recognized as a consequence of specific purposes, it does not recognize revenue until the condition is satisfied and the liability is reduced. As an entity satisfies a present obligation, it shall reduce the carrying amount of the liability recognized and recognize an amount of revenue equal to that reduction. Example: The NG received a foreign grant amounting to P10 million for the construction of a railroad system. Under the of the grant, the construction project shall be completed within a period of two years from the receipt of the grant, otherwise, the money shall be returned to the grantor. The money can only be used as stipulated and the NG is required to include a note in the financial statement detailing how the money was spent. The Department of Public Works and Highways (DPWH) will be the implementing entity.

a. Receipt of the Grant Books of the NG - BTr Cash in Bank-Local Currency, Bangko Sentral ng Pilipinas Other Deferred Credits To recognize receipt of grant Books of the Implementing NGA – DPWH Cash-Modified Disbursement System (MDS), Special Subsidy from National Government To recognize receipt of the NCA for a railroad system

P10,000,000 P10,000,000

P10,000,000 P10,000,000

b. Purchase of construction materials and payment for labor for the construction of a railroad system amounting to P10,000,000. Books of the Implementing NGA-DPWH Construction in Progress- Infrastructure Assets Cash-Modified Disbursement System, Special To recognize payment for the materials and labor

P10,000,000 P10,000,000

Books of the NG-BTr Subsidy from National Government Cash in Bank-Local Currency, Bangko Sentral ng Pilipinas To recognize replenishment of MDS checks

P10,000,000 P10,000,000

c. Receipt of the report from DPWH for the completion of the construction of a railroad system amounting to P10,000,000. Books of the NG - BTr Other Deferred Credits Income from Grants and Donations in Cash To recognize the income from grants and donations

P10,000,000 P10,000,000

d. Turnover and Acceptance of Completed Infrastructure Asset Books of the Implementing NGA - DPWH Railway System Construction in Progress- Infrastructure Assets To recognize the turnover and acceptance

P10,000,000 P10,000,000

RECEIPT OF NOTICE OF CASH ALLOCATION Regular: Cash-Modified Disbursement System (MDS), Regular Subsidy from National Government To recognize receipt of NCA for Regular Agency Fund

XX XX

Special :

Cash-Modified Disbursement System (MDS), Special XX Cash-Treasury/Agency Deposit, Special XX To recognize receipt of NCA for Special Acct in the General Fund

NON-CASH AVAILMENT AUTHORITY s Payable Subsidy from National Government To recognize the receipt of NCAA

XX

TAX WITHHELD BY NGAS NGAs’ (withholding agency) Books Cash-Tax Remittance Advice XX Subsidy from National Government To recognize constructive receipt of NCA for TRA

XX

XX

Due to BIR XX Cash-Tax Remittance Advice XX To recognize constructive remittance to BIR of taxes withheld through TRA BIR Books Cash-Tax Remittance Advice XX Income Tax XX To recognize constructive receipt of taxes remitted by NGAs through TRA BTr Books Subsidy to NGAs XX Cash-Tax Remittance Advice XX To recognize constructive receipt of remittance of taxes by NGAs through TRA COLLECTIONS MADE ON BEHALF OF ANOTHER ENTITY/ NON-GOVERNMENT/ PRIVATE ORG NGAs Books (Collecting Agency) Cash-Collecting Officers XX Due to NGAs XX To recognize collection of fees Due to NGAs XX Cash-Collecting Officers XX To recognize remittance of collections to BTr BTr Books Cash in Bank-Local Currency, Savings XX Cash-Treasury/Agency Deposit, Trust To recognize receipt of remitted collections for UP-LRF

XX

Another Entity Books Cash-Treasury/Agency Deposit, Trust Trust Liabilities To recognize remitted collections by other NGAs

XX

INTRA-AGENCY AND INTER-AGENCY FUND TRANSFERS 1. Intra-entity Fund Transfer Cash-Collecting Officers XX Due to Central Office/ Bureaus/ Offices To recognize receipt of intra-entity fund transfer Cash-Treasury/Agency Deposit, Trust XX Cash-Collecting Officers To recognize remittance of collections to BTr 2. Inter-agency Fund Transfer Cash-Collecting Officers XX Due to NGAs/ LGUs/ GOCCs To recognize receipt of inter-entity fund transfer Cash-Treasury/Agency Deposit, Trust XX Cash-Collecting Officers To recognize remittance of collections to BTr

XX

XX

XX

XX

XX

DISBURSEMENTS Notice of Cash Allocation. The NCA shall be the authority of an agency to pay operating expenses, purchases of supplies and materials, acquisition of PPE, s payable, and other authorized disbursements through the issue of MDS checks, ADA or other modes of disbursements. Notice of Transfer of Allocation. The NTA shall be the authority of the regional and operating units to pay their operating expenses, purchases of supplies and materials, acquisition of PPE, s payable, and other authorized disbursements through the issue of MDS checks, ADA or other modes of disbursements. Disbursements by Check. Checks shall be drawn only on duly approved Disbursement Voucher (DV) or Payroll. These shall be used for payment of regular expenses which cannot be conveniently nor practically paid using the ADA or not authorized to be paid using the Petty Cash Fund or advances for operating expenses. a. Modified Disbursement System Checks – are checks issued by government agencies chargeable against the of the Treasurer of the Philippines, which are maintained with different MDS-GSBs.

b. Commercial Checks – are checks issued by NGAs chargeable against the Agency Checking with GSBs. These shall be covered by income/receipts authorized to be deposited with AGDBs. Illustrative ing Entries for Disbursements By Check 1. Payment of the following utility bills: Meralco Bill P1,200 PLDT Bill 500 Maynilad Bill 200 Total P 1,900 Water Expenses Electricity Expenses Telephone Expenses Cash-Modified Disbursement System (MDS), Regular To recognize payment of bills from utility companies 2. Grant of cash advance for travel Advances to Officers and Employees Cash-Modified Disbursement System (MDS), Regular To recognize granting of travel allowance to employees 3. Advance payment to Procurement Service Due from NGAs Cash-Modified Disbursement System (MDS), Regular To recognize advance payment to Procurement Service for the purchase of Office Equipment

200 1,200 500 P 1,900

P 1,000 P 1,000

P 2,500 P 2,500

4. Establishment of Petty Cash Fund (PCF) – P 20,000 Petty Cash Fund P 20,000 Cash-Modified Disbursement System (MDS), Regular P 20,000 To recognize establishment of PCF to cover petty expenses 5. Replenishment of PCF Expenses charged to the PCF: Bond paper P 14,000 Postage stamps 2,000 Total P 16,000 Office Supplies Expenses Postage and Courier Expenses Cash-Modified Disbursement System (MDS), Regular To recognize replenishment of PCF

P 14,000 2,000 P 16,000

6. Remittance of Government’s share Retirement and Life Insurance Pag-IBIG Contributions PhilHealth Contributions Total

P 3,300 500 300 P 4,100

Retirement and Life Insurance s Pag-IBIG Contributions PhilHealth Contributions Cash-Modified Disbursement System (MDS), Regular To recognize remittance of government’s share 7. Remittance of salary deductions Retirement and Life Insurance Pag-IBIG Contributions PhilHealth Contributions GSIS-Salary Loan Employees' Association Total

P 3,300 500 300 P 4,100

P 3,300 500 300 200 100 P 4,400

Due to GSIS Due to Pag-IBIG Due to PhilHealth Other Payables 2 Cash-Modified Disbursement System (MDS), Regular To recognize remittance of salary deductions

P 3,500 500 300 100 P 4,400

safekeeping thereof in conformity with law. Every AO shall be properly bonded in accordance with law. c. Liability over Government Funds and Property Expenditures of government funds or uses of government property in violation of law or regulations shall be a personal liability of the official or employee found to be directly responsible therefor. Every officer able for government funds shall be liable for all losses resulting from the unlawful deposit, use, or application thereof and for all losses attributable to negligence in the keeping of the funds. FUNDAMENTAL PRINCIPLES FOR REVENUE a. Unless otherwise specifically provided by law, all revenues accruing to an entity by virtue of the provisions of existing law, orders and regulations shall be deposited/ remitted in the National Treasury (NT) or in any duly authorized government depository, and shall accrue to the General Fund (GF) of the NG. b. Amounts received in trust and from business-type activities of government may be separately recorded and disbursed in accordance with such rules and regulations as may be determined by a Permanent Committee composed of the Secretary of Finance as Chairman, and the Secretary of Budget and Management and the Chairman, COA, as . c. Receipts shall be recorded as revenue of Special, Fiduciary or Trust Funds or Funds other than the GF, only when authorized by law as implemented by rules and regulations issued by the Permanent Committee. d. No payment of any nature shall be received by a collecting officer without immediately issuing an official receipt in acknowledgement thereof. FUNDAMENTAL PRINCIPLES FOR DISBURSEMENT OF PUBLIC FUNDS a. No money shall be paid out of any public treasury or depository except in pursuance of an appropriation law or other specific statutory authority. b. Government funds or property shall be spent or used solely for public purposes. c. Trust funds shall be available and may be spent only for the specific purpose for which the trust was created or the funds received. d. Claims against government funds shall be ed with complete documentation. BASIC GOVERNMENT ING AND BUDGET REPORTING PRINCIPLES a. Generally accepted government ing principles in accordance with the PPSAS and pertinent laws, rules and regulations; b. Accrual basis of ing in accordance with the PPSAS;

c. Budget basis for presentation of budget information in the financial statements (FSs) in accordance with PPSAS 24; d. Revised Chart of s prescribed by COA; e. Double entry bookkeeping; f. Financial statements based on ing and budgetary records; and g. Fund cluster ing. Keeping of the General s The COA shall keep the general s of the Government and, for such period as may be provided by law, preserve the vouchers and other ing papers pertaining thereto Financial Reporting System for the National Government a. Each entity of the National Government (NG) maintains complete set of ing books by fund cluster which is reconciled with the records of cash transactions maintained by the BTr. b. Each entity maintains budget registries which are reconciled with the budget records maintained by the DBM and the Government ancy Sector (GAS), COA. c. The COA, through the GAS: 1. Maintains budget records showing the overall approved budget of the NG and its execution/implementation; 2. Consolidates the FSs and budget ability reports of all NGAs and the BTr with COA’s records to come up with an Annual Financial Report (AFR) for the NG as required in Section 4, Article IX-D of the 1987 Philippine Constitution; and 3. prepares other financial reports required by law for submission to oversight agencies. Components of General Purpose Financial Statements a. Statement of Financial Position b. Statement of Financial Performance c. Statement of Changes in Net Assets/Equity d. Statement of Cash Flows e. Statement of Comparison of Budget and Actual Amounts f. Notes to the Financial Statements, comprising a summary of significant ing policies and other explanatory notes Books of s and Registries a. Journals 1. General Journal

2. Cash Receipts Journal 3. Cash Disbursements Journal 4. Check Disbursements Journal b. Ledgers 1. General Ledgers 2. Subsidiary Ledgers c. Registries 1. Registries of Revenue and Other Receipts 2. Registry of Appropriations and Allotments 3. Registries of Allotments, Obligations and Disbursements 4. Registries of Budget, Utilization and Disbursements FUND ING: FUND CLUSTERS Code 01 02 03 04 05 06 07

Description Regular Agency Fund Foreign Assisted Projects Fund Special -Locally Funded/Domestic Grants Fund Special -Foreign Assisted/Foreign Grants Fund Internally Generated Funds Business Related Funds Trust Receipts

OTHER PROVISIONS a. Fair Presentation b. Compliance with PPSASs. Explicit and unreserved statement of such compliance c. Departure with PPSASs. If compliance with the requirement of PPSAS would result in misleading presentation that it would contradict the objective of the FSs set forth in PPSAS. d. Going Concern. Unless there is an intention to discontinue the entity operation, or if there is no realistic alternative but to do so. e. Consistency of Presentation. Retained from one period to the next unless laws, rules and regulations, and PPSAS require a change in presentation. f. Offsetting. Assets and liabilities, and revenue and expenses shall not be allowed to offset unless required or permitted by a PPSAS except when offsetting reflects the substance of the transaction or other event.

g. Comparative Information. Comparative information shall be disclosed with respect to the previous period for all amounts reported in the FSs. Comparative information shall be included for narrative and descriptive information when it is relevant to an understanding of the current period’s FSs. Inclusions in the Statement of Changes in Net Assets/ Equity a. Net Income or Deficit for the period; b. Each item of revenue and expenses for the period that, as required by Standards, is recognized directly in net assets/equity, and the total of these items; c. Total revenue and expenses for the period; and d. For each component of net assets/equity separately disclosed, the effects of changes in ing policies and corrections of errors recognized in accordance with PPSAS 3ing Policies, Changes in ing Estimates and Errors. Statement of Comparison of Budget and Actual Amounts. A comparison of budget and actual amounts will enhance the transparency of financial reporting in government. This shall be presented by government agencies as a separate additional financial statement referred in this Manual as the Statement of Comparison of Budget and Actual Amounts (SCBAA). Use of Appropriated Funds. All moneys appropriated for functions, activities, projects and programs shall be available solely for the specific purposes for which these are appropriated. Appropriation for Loan Proceeds. Expenditures funded by foreign and domestic borrowings shall be included within the expenditure program of the entity concerned. Loan proceeds, whether in cash or in kind, shall not be used without the corresponding release of funds through a Special Budget. Basic Requirements for Disbursements and the Required Certifications a. Availability of allotment/budget for obligation/utilization certified by the Budget Officer/Head of Budget Unit; b. Obligations/Utilizations properly charged against available allotment/budget by the Chief ant/Head of ing Unit; c. Availability of funds certified by the Chief ant; d. Availability of cash certified by the Chief ant; e. Legality of the transactions and conformity with existing rules and regulations. f. Submission of proper evidence to establish validity of the claim. g. Approval of the disbursement by the Head of Agency or by his duly authorized representative.

Mode of Disbursements. Payments/Disbursements by NGAs may be effected through the Treasury Single (TSA), by issuing Modified Disbursements System (MDS) check or commercial check, cash through cash advance, Advice to Debit (ADA), or Non-Cash Availment Authority (NCAA). NGAs are authorized to disburse/pay based on the Notice of Cash Allocation (NCA), Notice of Transfer of Allocation (NTA), Cash Disbursement Ceiling (CDC) or other authority that may be provided by law. BUDGET EXECUTION, MONITORING AND REPORTING Allotment – is an authorization issued by the DBM to NGAs to incur obligations for specified amounts contained in a legislative appropriation in the form of budget release documents. It is also referred to as Obligational Authority. Appropriation – is the authorization made by a legislative body to allocate funds for purposes specified by the legislative or similar authority. Disbursements – are the actual amounts spent or paid out of the budgeted amounts. Obligation – is an act of a duly authorized official which binds the government to the immediate or eventual payment of a sum of money. Obligation maybe referred to as a commitment that encomes possible future liabilities based on current contractual agreement. FUND RELEASE DOCUMENTS a. Obligational Authority or Allotment 1. General Appropriations Act Release Document (GAARD) – serves as the obligational authority for the comprehensive release of budgetary items appropriated in the GAA, categorized as For Comprehensive Release (FCR). 2. Special Allotment Release Order (SARO) – covers budgetary items under For Later Release (FLR) (negative list) in the entity submitted Budget Execution Documents (BEDs), subject to compliance of required documents/clearances. Releases of allotments for Special Purpose Funds (SPFs) (e.g., Calamity Fund, Contingent Fund, E-Government Fund, Feasibility Studies Fund, International Commitments Fund, Miscellaneous Personnel Benefits Fund and Pension and Gratuity Fund) are also covered by SAROs. 3. General Allotment Release Order (GARO) – is a comprehensive authority issued to all national government agencies, in general, to incur obligations not exceeding an authorized amount during a specified period for the purpose indicated therein.

b. Disbursement Authority 1. Notice of Cash Allocation (NCA) – authority issued by the DBM to central, regional and provincial offices and operating units to cover the cash requirements of the agencies; 2. Non-Cash Availment Authority (NCAA) – authority issued by the DBM to agencies to cover the liquidation of their actual obligations incurred against available allotments for availment of proceeds from loans/grants through supplier’s credit/constructive cash; 3. Cash Disbursement Ceiling (CDC) – authority issued by DBM to the Department of Foreign Affairs and Department of Labor and Employment to utilize their income collected/retained by their Foreign Service Posts (FSPs) to cover their operating requirements, but not to exceed the released allotment to the said post; and 4. Notice of Transfer of Allocation – authority issued by the Central Office to its regional and operating units to cover the latter’s cash requirements. Registry of Appropriations and Allotments Shall be maintained by NGAs to monitor appropriations and allotments charged thereto. It shall show the original, supplemental and final budget for the year and all allotments received charged against the corresponding appropriation. Registries of Budget, Utilization and Disbursements Shall be used to record the approved special budget and the corresponding utilizations and disbursements charged to retained income authorized under R.A. 8292 for SUCs and other retained income collection of a national government agency with similar authority, Revolving Funds and Trust Receipts/Custodial Funds. a. Registry of Budget, Utilization and Disbursements-Personnel Services (RBUD-PS) shall be used to record the budget utilizations and disbursements classified under PS. b. Registry of Budget, Utilization and Disbursements-Maintenance and Other Operating Expenses (RBUD-MOOE) shall be used to record the budget utilizations and disbursements classified under MOOE. c. Registry of Budget, Utilization and Disbursements-Financial Expenses (RBUD-FE) shall be used to record the budget utilizations and disbursements classified under FE. d. Registry of Budget, Utilization and Disbursements-Capital Outlays (RBUD-CO) shall be used to record the budget utilizations and disbursements classified under CO.

Budget Utilization Request and Status. The incurrence of budget utilization shall be made through the issuance of Budget Utilization Request and Status (BURS). The BURS shall be prepared by the Requesting/Originating Office ed by valid claim documents like DV, payroll, purchase/job order, itinerary of travel, etc. Presentation of Budget Information in the Financial Statements on a Comparable Basis. An entity shall prepare a comparison of the budget and actual amounts spent as a separate statement since the budget and the financial statements are not prepared on a comparable basis in accordance with PPSAS Responsibility Center Code Structure. Each NGA shall be assigned a responsibility center code defined as organization code in the UACS Manual. For monitoring revenue and expenses, additional three digit codes for the agency’s major offices/departments shall be appended to the organization code. The organization code and the agency’s major offices/departments’ code shall consist of 15 digits as follows:

REVENUE AND OTHER RECEIPTS Unless otherwise specifically provided by law, all revenue (income) accruing to the departments, offices and agencies by virtue of the provisions of existing laws, orders and regulations shall be deposited in the NT or in the duly authorized depository of the Government and shall accrue to the General Fund of the Government: Provided, that amounts received in trust and from business-type activities of government may be separately recorded and disbursed in accordance with such rules and regulations as may be determined by the Permanent Committee. Revenue from Exchange Transactions 1. Rendering of services 2. Sale of goods 3. Interests 4. Royalties 5. Dividends or similar distributions Revenue from Non-Exchange Transactions a. Tax Revenue- Individual and Corporation, Property, Goods and Services, Others b. Fines and Penalties- Tax Revenue, Service Income, Business Income c. Shares, Grants and Donations- Share from National Wealth, Share from Philippine Amusement and Gaming Corporation (PAGCOR)/ Philippine Charity Sweepstakes Office (PCSO), Share from Earnings of GOCCs, Income from Grants and Donations in Cash, Income from Grants and Donations in Kind d. Revenues arising from Trust Liabilities, Deferred Credits, Unearned Revenue GRANT WITH CONDITION If conditions are attached to a grant, a liability is recognized. If the government is required to recognize a liability in respect of any conditions relating to assets recognized as a consequence of specific purposes, it does not recognize revenue until the condition is satisfied and the liability is reduced. As an entity satisfies a present obligation, it shall reduce the carrying amount of the liability recognized and recognize an amount of revenue equal to that reduction. Example: The NG received a foreign grant amounting to P10 million for the construction of a railroad system. Under the of the grant, the construction project shall be completed within a period of two years from the receipt of the grant, otherwise, the money shall be returned to the grantor. The money can only be used as stipulated and the NG is required to include a note in the financial statement detailing how the money was spent. The Department of Public Works and Highways (DPWH) will be the implementing entity.

a. Receipt of the Grant Books of the NG - BTr Cash in Bank-Local Currency, Bangko Sentral ng Pilipinas Other Deferred Credits To recognize receipt of grant Books of the Implementing NGA – DPWH Cash-Modified Disbursement System (MDS), Special Subsidy from National Government To recognize receipt of the NCA for a railroad system

P10,000,000 P10,000,000

P10,000,000 P10,000,000

b. Purchase of construction materials and payment for labor for the construction of a railroad system amounting to P10,000,000. Books of the Implementing NGA-DPWH Construction in Progress- Infrastructure Assets Cash-Modified Disbursement System, Special To recognize payment for the materials and labor

P10,000,000 P10,000,000

Books of the NG-BTr Subsidy from National Government Cash in Bank-Local Currency, Bangko Sentral ng Pilipinas To recognize replenishment of MDS checks

P10,000,000 P10,000,000

c. Receipt of the report from DPWH for the completion of the construction of a railroad system amounting to P10,000,000. Books of the NG - BTr Other Deferred Credits Income from Grants and Donations in Cash To recognize the income from grants and donations

P10,000,000 P10,000,000

d. Turnover and Acceptance of Completed Infrastructure Asset Books of the Implementing NGA - DPWH Railway System Construction in Progress- Infrastructure Assets To recognize the turnover and acceptance

P10,000,000 P10,000,000

RECEIPT OF NOTICE OF CASH ALLOCATION Regular: Cash-Modified Disbursement System (MDS), Regular Subsidy from National Government To recognize receipt of NCA for Regular Agency Fund

XX XX

Special :

Cash-Modified Disbursement System (MDS), Special XX Cash-Treasury/Agency Deposit, Special XX To recognize receipt of NCA for Special Acct in the General Fund

NON-CASH AVAILMENT AUTHORITY s Payable Subsidy from National Government To recognize the receipt of NCAA

XX

TAX WITHHELD BY NGAS NGAs’ (withholding agency) Books Cash-Tax Remittance Advice XX Subsidy from National Government To recognize constructive receipt of NCA for TRA

XX

XX

Due to BIR XX Cash-Tax Remittance Advice XX To recognize constructive remittance to BIR of taxes withheld through TRA BIR Books Cash-Tax Remittance Advice XX Income Tax XX To recognize constructive receipt of taxes remitted by NGAs through TRA BTr Books Subsidy to NGAs XX Cash-Tax Remittance Advice XX To recognize constructive receipt of remittance of taxes by NGAs through TRA COLLECTIONS MADE ON BEHALF OF ANOTHER ENTITY/ NON-GOVERNMENT/ PRIVATE ORG NGAs Books (Collecting Agency) Cash-Collecting Officers XX Due to NGAs XX To recognize collection of fees Due to NGAs XX Cash-Collecting Officers XX To recognize remittance of collections to BTr BTr Books Cash in Bank-Local Currency, Savings XX Cash-Treasury/Agency Deposit, Trust To recognize receipt of remitted collections for UP-LRF

XX

Another Entity Books Cash-Treasury/Agency Deposit, Trust Trust Liabilities To recognize remitted collections by other NGAs

XX

INTRA-AGENCY AND INTER-AGENCY FUND TRANSFERS 1. Intra-entity Fund Transfer Cash-Collecting Officers XX Due to Central Office/ Bureaus/ Offices To recognize receipt of intra-entity fund transfer Cash-Treasury/Agency Deposit, Trust XX Cash-Collecting Officers To recognize remittance of collections to BTr 2. Inter-agency Fund Transfer Cash-Collecting Officers XX Due to NGAs/ LGUs/ GOCCs To recognize receipt of inter-entity fund transfer Cash-Treasury/Agency Deposit, Trust XX Cash-Collecting Officers To recognize remittance of collections to BTr

XX

XX

XX

XX

XX

DISBURSEMENTS Notice of Cash Allocation. The NCA shall be the authority of an agency to pay operating expenses, purchases of supplies and materials, acquisition of PPE, s payable, and other authorized disbursements through the issue of MDS checks, ADA or other modes of disbursements. Notice of Transfer of Allocation. The NTA shall be the authority of the regional and operating units to pay their operating expenses, purchases of supplies and materials, acquisition of PPE, s payable, and other authorized disbursements through the issue of MDS checks, ADA or other modes of disbursements. Disbursements by Check. Checks shall be drawn only on duly approved Disbursement Voucher (DV) or Payroll. These shall be used for payment of regular expenses which cannot be conveniently nor practically paid using the ADA or not authorized to be paid using the Petty Cash Fund or advances for operating expenses. a. Modified Disbursement System Checks – are checks issued by government agencies chargeable against the of the Treasurer of the Philippines, which are maintained with different MDS-GSBs.

b. Commercial Checks – are checks issued by NGAs chargeable against the Agency Checking with GSBs. These shall be covered by income/receipts authorized to be deposited with AGDBs. Illustrative ing Entries for Disbursements By Check 1. Payment of the following utility bills: Meralco Bill P1,200 PLDT Bill 500 Maynilad Bill 200 Total P 1,900 Water Expenses Electricity Expenses Telephone Expenses Cash-Modified Disbursement System (MDS), Regular To recognize payment of bills from utility companies 2. Grant of cash advance for travel Advances to Officers and Employees Cash-Modified Disbursement System (MDS), Regular To recognize granting of travel allowance to employees 3. Advance payment to Procurement Service Due from NGAs Cash-Modified Disbursement System (MDS), Regular To recognize advance payment to Procurement Service for the purchase of Office Equipment

200 1,200 500 P 1,900

P 1,000 P 1,000

P 2,500 P 2,500

4. Establishment of Petty Cash Fund (PCF) – P 20,000 Petty Cash Fund P 20,000 Cash-Modified Disbursement System (MDS), Regular P 20,000 To recognize establishment of PCF to cover petty expenses 5. Replenishment of PCF Expenses charged to the PCF: Bond paper P 14,000 Postage stamps 2,000 Total P 16,000 Office Supplies Expenses Postage and Courier Expenses Cash-Modified Disbursement System (MDS), Regular To recognize replenishment of PCF

P 14,000 2,000 P 16,000

6. Remittance of Government’s share Retirement and Life Insurance Pag-IBIG Contributions PhilHealth Contributions Total

P 3,300 500 300 P 4,100

Retirement and Life Insurance s Pag-IBIG Contributions PhilHealth Contributions Cash-Modified Disbursement System (MDS), Regular To recognize remittance of government’s share 7. Remittance of salary deductions Retirement and Life Insurance Pag-IBIG Contributions PhilHealth Contributions GSIS-Salary Loan Employees' Association Total

P 3,300 500 300 P 4,100

P 3,300 500 300 200 100 P 4,400

Due to GSIS Due to Pag-IBIG Due to PhilHealth Other Payables 2 Cash-Modified Disbursement System (MDS), Regular To recognize remittance of salary deductions

P 3,500 500 300 100 P 4,400

Related Documents 2w1qw

Government ing Manual For National Government Agencies 4w695u

November 2019 131

Government ing Manual For Ngas 606q3a

October 2020 0

Government ing 3a4971

December 2019 46

Government ing Manual 371q8

February 2022 0

Government ing . ing Responsibilities. 3w1l58

November 2019 103

Government ing In Bangladesh 3f1c1q

October 2021 0More Documents from "Kenneth Calzado" 116n1p

Business Combination Notes 4k54q

April 2020 24

Government ing Manual For National Government Agencies 4w695u

November 2019 131

504uu

May 2021 0

504uu

November 2019 26

Business Ethics: Managing Corporate Citizenship And Sustainability In The Age Of Globalization j6w1p

October 2020 0